COALspot.com: The Indonesia coal benchmark price hits to its highest level since August 2015.

The Director General of Mineral and Coal of Indonesia, the regulator of Coal industry in Indonesia who has authority to declare the monthly benchmark price for Indonesian thermal coal, had declared August 2016 HBA at US$ 58.37 per ton for 6322 GAR power plant coal.

DGoMC has increased the Indonesian thermal coal price reference for August delivery by 10.13% a ton. This increase is the highest average monthly price gain since February 2011.

In the meantime, the August 2016 HBA was 1.30% lesser the comparable period in 2015.

The Indonesian coal price reference of August 2016 raised US$ 5.37 a ton from July 2016. An increase or decrease in four international coal indices such as ICI-1, Platts-5900, NEX and GC will cause an increase or decrease in Indonesian coal price reference every month, as HBA is linked to those indices.

The coal price reference in Indonesia was established to fulfil the requirement of mining law 04/2009 and ministerial decree No.17/2010. In addition to that, it aims to increase government revenue from royalties from coal producers.

According to the data from Director General shows that the government has fixed US$ 14.42 a ton (up 10.08% month on month) for the coal with calorific value 2,995 kcal/kg on GAR with total moisture 50.10% on as received basis for August 2016 FOB vessel delivery. In the meantime, the government is also declared US$ 42.42 per ton as HPB for 5000 GAR coal with total moisture 22.40%, Ash 8.90% and Sulphur 0.54% for August 2016 deliveries.

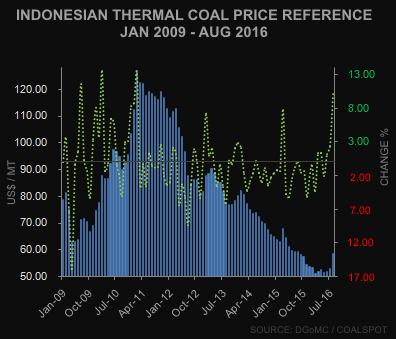

The declared Indonesia thermal coal reference price for February 2016 (or called HBA) was the lowest in 92 months or since launching of HBA by the government of Indonesia. The royalty and taxes will be calculated based on this declared HPB.

Indonesian coal benchmark price for August 2016 was calculated based on calorific value of 6,322 kcal/kg (GAR), stated to be using a formula based on the July 2016 index average of ICI-1 (Indonesia Coal Index) 25%, Platts-5900 25%, NEX (Newcastle Export Index) 25%, and GC (globalCoal Index) 25% and its was calculated considering coal with GCV (GAR) 6,322 kcal/kg, Total Moisture (arb) 8.00%, Total Sulphur 0.8% (arb), Ash Content 15 % (arb) and delivery free on Board (FOB) Vessel basis and apply to spot contract, delivery between 1 – 31 August 2016.

The highest benchmark price was declared by the Ministry of Energy & Mineral Resources of Indonesia in February 2011, and this month declared price is around US$ 68.68 a ton or 54.05 per cent lower compared to Feb’ 11 benchmark price.

The government of Indonesia was publishing a monthly coal price reference (HBA & HPB) since January 2009 to be used by coal producers for all spot and term contracts.

However, the official implementation of HBA was commenced since September 2011 and according to government regulation, the coal benchmark price must be used by the holders of production operation IUPs, special production operation IUP's, and CCoWs as a reference in determining the coal selling price for a particular period.

HBA of February 2011 was the highest since the launching of HBA by the government of Indonesia (US$ 127.05 / MT for 6322 GAR coal) and the lowest was declared in February 2016 (US$ 50.92 / MT).

The declared HBA in this month is valid for the spot price (loading on or before 31 August 2016), while as for term price (up to 12 months supply), the average reference price (HPB) of the previous three months will be used to determine the selling price. (50% of the latest available month's HPB (this month) 30% one month prior HPB and 20% of two-month prior HPB).

The government is also declaring the price marker for eight brands of Indonesia's coal, which are most commonly traded in the market. Those eight brands act as the benchmark and used to calculate other 67 coal types with a quality similar to the coal price markers.

Indonesian coal prices are starting to zoom higher and slowly moving towards North. The market players are forecasting that, the coal prices will likely surge further in 2016 as the recent price movement suggesting that the market has overcome the bearish trend which disturbed the industry for a very long period.

The coal market was oversupplied due to high production and sluggish demand for coal consuming countries in the past few months or years. Even thou the oversupply issue was still not vanished away completely, the current levels of coal output are still huge, but the recent changes in coal producing countries except India are definitely indicating a tightening on output. The tight market is expected to drive the coal prices further up in the coming weeks/ months unless the China reduces its control on tight production policy and change its buying pattern.

The lack of new demand, fast developments of renewable energy and attractive Gas prices is still to be blamed for obstacle of faster coal price recovery. Unless a permanent and meaningful supply-and-demand equation created, the prices won’t rebound meaningfully and for the time being the market will continue as a buyer's market and giving buyers an advantage over sellers in price negotiations.

Click here for full details of Indonesian coal price reference since January 2009

.(cs)

COALspot.com makes no warranties, express or implied, as to the accuracy adequacy or completeness of the information and assumes no liability in connection with any party use of it. The information contained within the website of COALspot.com is intended for informational purposes only and is not intended as professional counsel and should not be used as such.

COALspot.com will endeavour to update information where appropriate, but is under no obligation to do so. All third party users of this website and or data produced or published by the COALspot.com do so at their own risk.